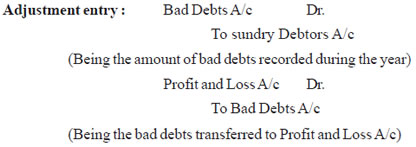

7. Bad Debts : The amount which can't be recovered from the debtor is known as bad debts.

Accounting Treatment : (i) The amount of bad debts will be debited to profit and loss account. If bad debts is already given in trial balance and further bad debts given in additional information, then further bad debt will be added in the debts in P and L A/c Dr. Side.

(ii) The amount of sundry debtor will be reduced by the amount of bad debts in the Assets side of Balance Sheet.

Note : If bad debt given only in trial balance then it is to be debited to

P & L A/c Only.8. Provision of Doubtful Debts : A provision is created to cover any possible loss on account of bad debts likely to occur in future. Generally, such a provisionis created at a fixed percentage on debtor at end of every year and it is called 'Provision of doubtful debts'.

Note : A Provision for doubtful debts is made always ondebtor after deducting the amount of bad debts given in adjustment.

Case 1. When provision for doubtful debts is not appearing on the Trial Balance.

Profit and Loss A/c Dr.

To Provision for doubtful debts A/c.

(Being provision made on debtors)Note : In this case provision for doubtfu debts will be debited to Profit and Loss A/c and Amount of debtors will reduced by it.

Case 2. When Provision for doubtfur debts is appearing in Trial Balance. (Old Provision)

Accounting Entries : (old + New Bad debts)

(i) For adjusting bad debts ( old + New Bad Debts) Provision for doubtful debts A/c Dr.

To Bad Debts A/c

(Being bad debts written from old provision)(ii) for creating New provision : with the amount of difference : Profit and Loss A/c Dr.

To Provision for doubtful debts A/c

(New provision debts [old Provision total Bad debts] )Illustration No. 7.

Additional Infomation : Further Bad Debts amounted Rs. 1,000 and create provision for Doubtful Debts @ 5%.

Profit and Loss Account for the year ended......

CBSE Accountancy Class XI ( By Mr. Aniruddh Maheshwari )

Email Id : [email protected]