14. Insolvency of Acceptor –

When the drawee (i.e., acceptor) of a bill is unable to meet his liabilities on due date, the drawee become insolvent. In such a case, entries for the dishonour of the bill are passed in the books of drawer/holder and drawee of the bill.

Any protortionate amount received from the drawee is recorded in the books of the holder and the amount unrecoverable is debited to 'Bad Debts A/c'.

Accounting Treatment of Bill Transactions

A. On the Due Date bill is Honoured –

The accounting treatment under this heading is based on the assumption that bill is duly honoured at maturity of the bill. The drawer can treat the bill in the following

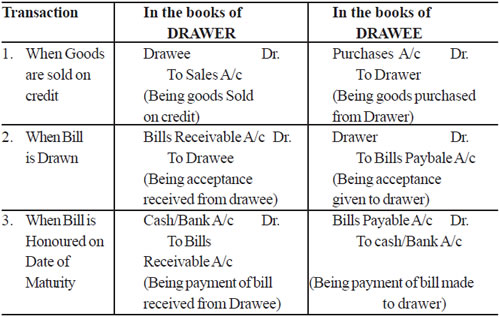

ways :Case - I Bill is retained by the drawer till date of maturity

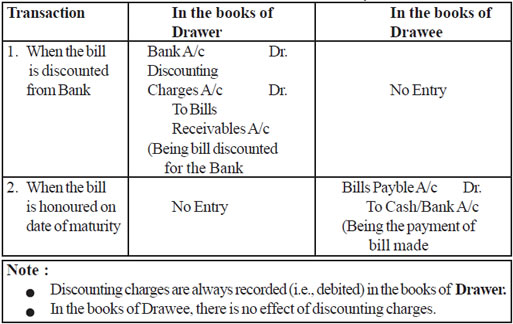

Case II : When the bill is discounted from the Bank by the Drawer

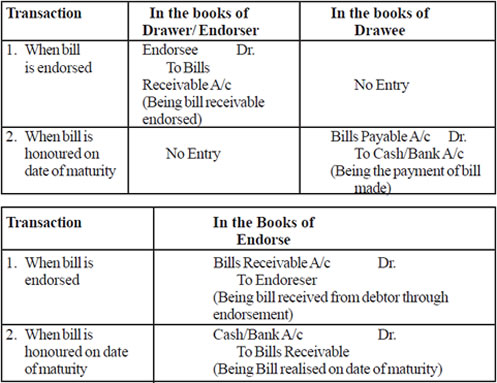

Case III : When bill is endorsed in favour of a creditor

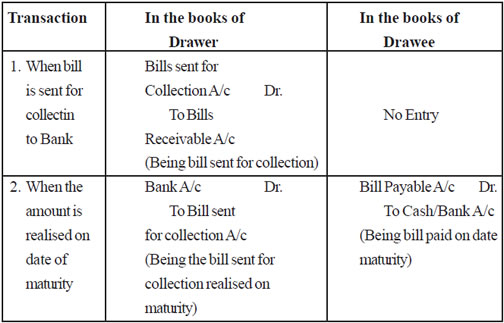

Case - IV When Bill is sent to the Bank for collection

Note :

There will be no effect in the books of Drawee either the bill is discounted from the bank or endorsed to a creditor or sent to the bank for collection. The drawee makes the payment in normal manner.

It is only in the books of drawer where an additional entry is passed to record the effect of the above transaction.

CBSE Accountancy Class XI ( By Mr. Aniruddh Maheshwari )

Email Id : [email protected]