Important :

Rectification of double sided errors can easily be understood by the students.

There are rectified by passing the journal entries as given above irrespective of the

time of defiction of the errors.RECTIFICATION OF ONE SIDED ERRORS

These errors affect only one side of an Account either debit or credit. Therefore

these errors affect the Trial Balance. Rectification of these errors is done difference in the two cases i.e.(i) Before preparing the Trial Balance

(ii) After praparing the Trial Balance

Casse I : Rectification of one sided errors before preparing Trial Balance.

When there errors are rectified before preparing Trial Balance i.e transfering the difference in the Trial Balance to the Suspense Account.

(Which will be explained later on), then it is done directly by debiting or crediting the concerned ledger account.

For short Debit → Concerned A/c is Debited

For Excess Credit → Concerned A/c is Debited

For Short Credit → Concerned A/c is Credited

For Excess Debit → Concerned A/c is Credited

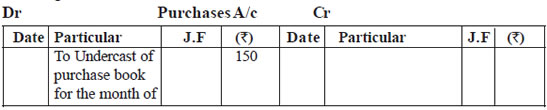

Example : (1) Purchase Book undercast by Rs. 150

Analysis : It means that the total of the Purchase Book is Rs. 150 short.

Here debit side of the Purchase A/c was short therefore the rectifcation is done by debiting the A/c.

Example 2 - Purchase Book is overcast by Rs. 300

Analysis

Here debit side of the purchases A/c was in exces, therefore the recification is done by entering the amount on the opposite side i.e. Credit side of the Purchases A/c.

Case II : Rectification of one Sided Error after Preparing Trial Balance

When the errors are detected after the preparetion of Trial Balance then every single sided error is rectified by passing a Journal entry through the Suspense Account.

For short Debit in one Account → Debit that Account and Credit the Suspense

A/c

Excess Credit in one Account Debit that Account and Credit the Suspense A/c

Short Credit in one Account → Credit that A/c and Debit the Suspense A/c

Excess Debit in one Account → Credit that A/c and Debit the Suspense A/c

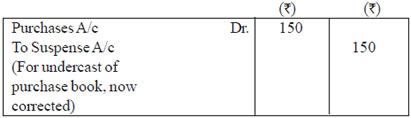

Example 3 : Hence for the same error as given in example No in case I, the

following Journal Entry will be passed.

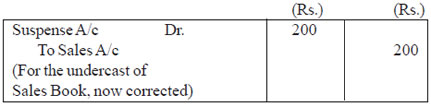

Example 4 : Sales Book was undercast by Rs. 200.

Analysis

Note :

When nothing is mentioned in the question about the time of detection of an error,

the students are advised to rectify one sided errors through Suspense A/c.

CBSE Accountancy Class XI ( By Mr. Aniruddh Maheshwari )

Email Id : [email protected]