Illustration 4 : Prepare a Cash book with Bank column from the following information :

2011 |

|

|

Jan. 1 |

Cash in hand |

12,000 |

Jan. 1 |

Bank Overdraft |

3,000 |

Jan. 5 |

Deposited into Bank |

2,000 |

Jan. 7 |

Received a cheque from Pujan |

10,000 |

Jan. 10 |

Goods sold for cash |

6,000 |

Jan. 12 |

Sold goods to Naveen |

7,000 |

Jan. 15 |

Received a Cheque from Naveen |

7,000 |

Jan. 20 |

Salary paid by cheque |

5,000 |

Jan. 21 |

Naveen’s cheque deposited into bank |

|

Jan. 25 |

Payment made to Shyam by cheque |

2,000 |

Jan. 30 |

Bank charged interest on overdraft |

100 |

Double Column Cash Book :

Date

Particulars

V.N.

L.F.

Cash

Bank

Date

Particular

V.N.

L.F.

Cash

Bank

2011

Jan. 1

Jan. 5

Jan. 7

Jan. 10

Jan. 15

Jan. 21

To Bal b/d

To Cash

To Pujan

To Sales

To Naveen

To Cash

C

C

12,000

6,000

7,000

2,000

10,000

7,000

2011

Jan. 1

Jan. 3

Jan. 20

Jan. 21

Jan. 25

Jan. 30

Jan. 31

By Bal b/d

By Bank

By Salary

By Bank

By Shyam

By Interest

By Bal c/d

C

C

2,000

7,000

16,000

3,000

5,000

2,000

100

8,900

25,000

19,000

25,000

19,000

2011

Feb. 1

To Bal b/d

16000

8900

Note :

PETTY CASH BOOK

Business has to incur small expenses which are repetitive in nature. To save the time and efforts of head cashier, business appoints a petty cashier. He is entrusted with the duty of paying these expenses.

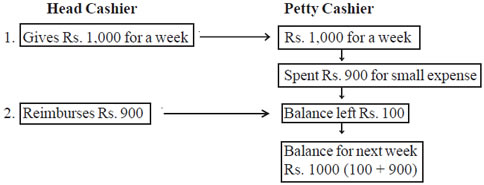

IMPREST SYSTEM OF PETTY CASH BOOK

Under this system, Head cashier gives a fixed amount to petty cashier for a definite period. At the end of given period, Head cashier reimburses the amount actually spent by the petty cashier resulting the same amount with petty cashier which he had in the beginning of the period. This can be illustrated as under.

Advantages of Petty Cash book

CBSE Accountancy Class XI ( By Mr. Aniruddh Maheshwari )

Email Id : [email protected]